My #1 Idea for 2025

About to make a move with this quality company?

This one cybersecurity company is spinning in my head.

Software companies aspire to achieve the famous ‘Rule of 40’:

→ 20% revenue growth + 20% Free Cash Flow, or a combination of the two.

Well, this company is among the rising leaders that is reshaping the rules of the game.

70 is the new 40. And as for the ‘Rule of 70’, they:

Have been growing +45% at 26% FCF → scoring 70+

Last quarter, they grew +26% at 46% FCF → scoring 73

Is Zscaler my next holding?

If you’re new, don’t miss out some of my recent updates:

Grab your coffee, and let’s find out together.

Understanding the Business

If I had to explain to a child my understanding of Zscaler, I would mention a few points:

The company is a pioneer of cloud-based secure internet access and it has grown into a market leader with a wide range of products and solutions

The company uses a "zero-trust" model, where every user, app, or device connects to its cloud platform individually, as if each were its own island

Unlike most competitors, Zscaler’s system isn’t one-to-many (with one central data center serving all devices). Instead, it’s one-to-one, making the system more agile, efficient, and user-friendly (see their slide below)

The company has rapidly expanded its service offerings over the years, maintaining a strong position at the forefront of innovation in cloud security.

While we could delve into each specific product in detail, for the sake of efficiency, I’ll share some infographics from their latest Investor Relations presentations.

Here’s a clear breakdown of their products categorized by client type:

Down below, a summary about their milestones and product launches:

Quality Indicators

If I’m bringing this company to your attention, it’s because it keeps popping up as quality name across several watchlists.

Here’s a recap for ZS 0.00%↑ :

✅ Founder-Led Company (2007)

✅ 114% Net Dollar Retention → If the company stopped onboarding new clients, it would still grow 14% y/y. On top, the company mentions an up to 6x upsell opportunity on existing clients.

✅ >70 Net Promoter Score

✅ 38.3% Insider Ownership → strong alignment between insiders and shareholders

✅ 23% R&D/Revenues: Innovation Champion → with strong innovation track record

✅ High Revenue Quality → Leader in a fast-growing, need-based industry with recurring revenue streams, multiple upselling opportunities, and new disruptive business segments

✅ Financial Health → Negative Net Financial Position, strong FCF (%), 81% Gross Margin

✅ Rule of 70 Champion → Leader in the SaaS space

✅ Awarded by Gartner as Security Leader

Over the past 5 years, the stock has returned an impressive 35% on average per year.

However, it’s still down -43% from the highs in 2021, and it has significantly underperformed in 2024 with a YTD performance of ‘only’ +6%.

Is the stock taking a break before a new break-out? As you know, I’m not a trader and I don’t look at charts to make my long-term oriented decisions.

But why hasn’t the stock kept the pace of a year-end market rally for US listed equities?

My 2cents is the following:

ZS is another symbol of the 2021 euphoria cycle, with its subsequent burst, and it is still on a recovery mode;

Wall Street may not like high stock-based compensations, weighting 20%-25% on revenue;

The company still exhibits negative GAAP Operating Margin;

The market got complacent with a post-Covid sales cycle with astonishing growth rates (50%-60% clip) that were clearly not sustainable.

2-Cents on the latest Earnings

Last Monday, ZS reported their Q1-25 earnings, and the stock was down -4%.

Despite triple beats on revenue, operating margin, and free cash flow, Wall Street did not like forward revenue guidance, pointing to a less explosive +21%/+22% growth projection.

As usual, the market gets complacent with past performance and pretends consistency for the future at the same time.

As we said, it seems pretty clear how the company can’t keep growing at the same pace of the last 3 years (+45%), mainly boosted by the Covid-effect.

Personally, I was positively impressed by 2 key numbers:

1) The higher-spending customers are growing much faster → This somehow confirms Management’s statement regarding upselling opportunities on already existing clients (up to 6x!).

2) Free Cash Flow jumping to 46% → They explain how this was possible thanks to higher billings collection in the quarter, plus lower CAPEX expenditure and lower SBC expenses as % of revenues. This is golden. It’s pure operating leverage, which is what we are typically looking for in Tech-related businesses.

My Business Case & Risk-Reward (Summary)

Zscaler is currently navigating through the funnel of my investing process:

✅ Does it live up to my quality standards? → yes

✅ Do I understand the business? → yes

In the following phases, we have:

❓Is it an attractive Risk-Reward?

❓Can the company achieve profitable growth?

❓Do I see major business or external risks?

❓Can I validate my risk-reward with a 5-year business case?

❓Am I experiencing any behavioral biases or emotional traps?

Here below I am providing some highlights taken from the various steps.

Business Case

When I’m diving deep into a the business fundamentals of a quality company, I prepare a 3-scenario business plan (bear, base, bull) built on top of the income statement and around a few strategic business KPIs.

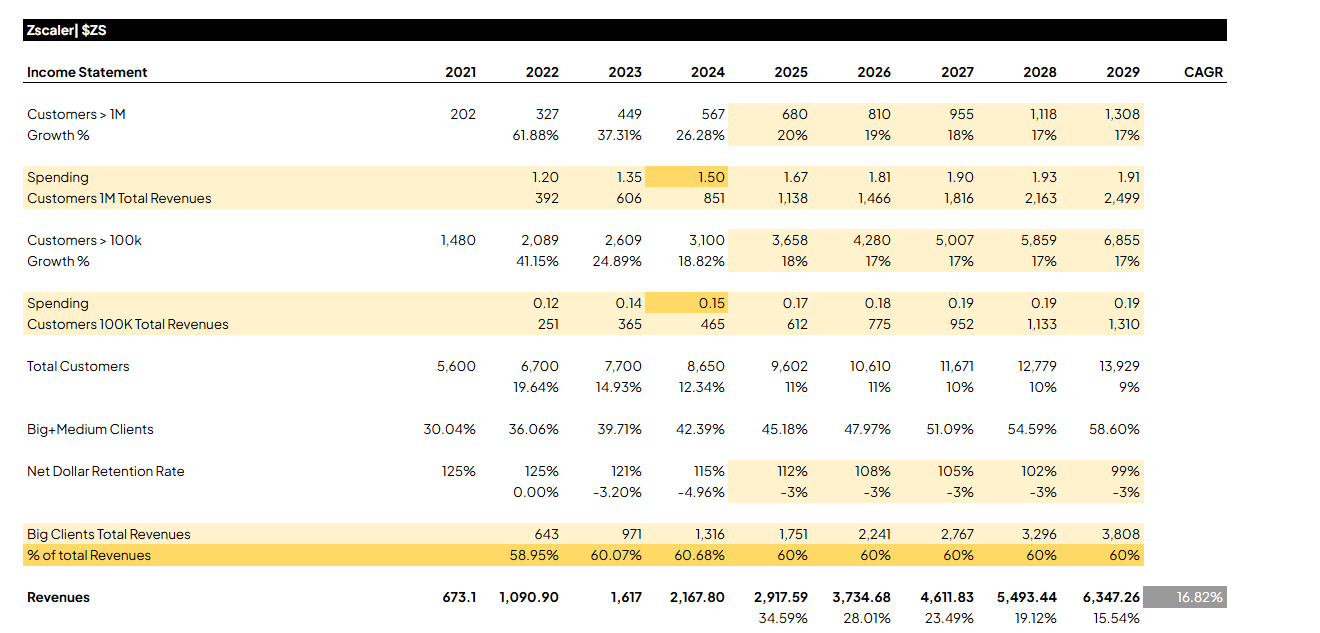

You can see an example of my bear case for Zscaler:

It wasn’t immediate to find the strateigic KPIs to pivot the business case around, but here’s the idea:

I broke down revenues by Client type:

> 1M Customers, spending on average $1.5M, $1.6M, or $1.65M (conservative assumptions)

> 100K Customers, spending on average $150K, $160K, or $165K (conservative assumption)

Sum of these 2 types of customers over total revenues: about 60% (the company does not disclose this data, which would have been super useful)

I projected Net Dollar Retention:

Falling -3% on average in the bear case

Falling -2% on average in the bear case

Falling -1% on average in the bull case (again, conservative)

Gross Margin stable at 81% over time (did I say conservative?)

SG&A and SBC costs decreasing in terms of incidence on Revenues, in line with recent developments and Management statements

Long-story short, I was able to come up with 3 revenue CAGR rates for the period 2025-2029:

🐻 17% | ⚖️ 22% | 🐂 24%

The Business Case continues with assumptions related to operating and other non-operating expenses, with one main question in mind. What are 3 reasonable net profit margins for 2029?

I won’t dive deep into that section, but the 3 net profit margins that I was able to come up with are:

🐻 17% | ⚖️ 21% | 🐂 34%

➡️ Result?

Plugging in these input variables into my automated Stock Predictor Tool, I finalized my Risk-Reward profile for Zscaler:

Summary:

➡️ The downside does not seem fully protected. However, I must admit that I built a pretty conservative bear case, that I will reassess;

➡️ The upside does give me an interesting price point above my target +15% average return per year;

➡️ I am experiencing a few mental biases that are keeping me from making my first move in a company I consider of extreme high quality:

Anchoring bias: in the past, I anchored myself to $150, and it sounds like I am still there mentally

Timing bias: given the weaker momentum, I am tempted to wait a bit longer to catch the stock below $200, ideally with an initial price point of $180

Analysis Paralysis + Confirmation Bias: I keep playing with numbers to find a combination that satisfies my downside. This is a danger!

All in all, I will wrap up my research coming this month, with the objective to make (or not to make) a calculated move in January.

Join me on the fun ride of equity investing

If you are looking to remove all the blocks that are keeping you from becoming a confident equity investor:

Time constraints (research & analysis take time and self-discipline, if you’re alone without a direction)

Information overload (where do I get the right info?)

Confusion on how to deal with stocks: when do I buy? when do I sell? How can I build scenarios?

➡️ Consider applying to The Investor’s Edge, my 1:1 Mentorship Program!

Within the 3+ month program, I will be happy to accelerate and add unique value to your investing journey with a proven risk-first, market-beating strategy and all the support tools that make the whole process very fast and reliable.

As Certified Financial Coach, Independent Investor with 33% return/year (despite many beginner mistakes!) since 1/1/2021, I would love lo lend a hand.

✅ Write me ‘Edge’ in the chat below to claim your spot.

I can’t wait to accompany motivated aspiring investors like you.

Very few spots left!

📈

Thank you again for your valuable time.

Happy Investing,

Francesco - Business Invest

Great analasys, however, I have a feeling that the market is going to crash in the next 2-3 months, everything seems expensive to me. I don't know where this feeling is coming from.

Great article, and a very interesting business. Well done!