If life gives you Lululemon...

is LULU a buying opportunity?

Down -45% Year-to-Date: is Lululemon a buying opportunity?

In today's episode:

I'll analyze key qualitative and quantitative metrics for Lululemon

I'll present a simplified business case exploring Lululemon's expansion opportunities

I'll briefly simulate what needs to happen to reasonably anticipate a 2x increase (+100%) in value from now by 2028

To keep the article short, I won’t delve into what the company does (I trust you are already familiar with it due to the popularity of the brand).

Let's dive in!

LULU’s Growth Strategy in 2 Numbers

This article was inspired by 2 numbers which seem to define the strategic growth plan of the company for the next years. What are they?

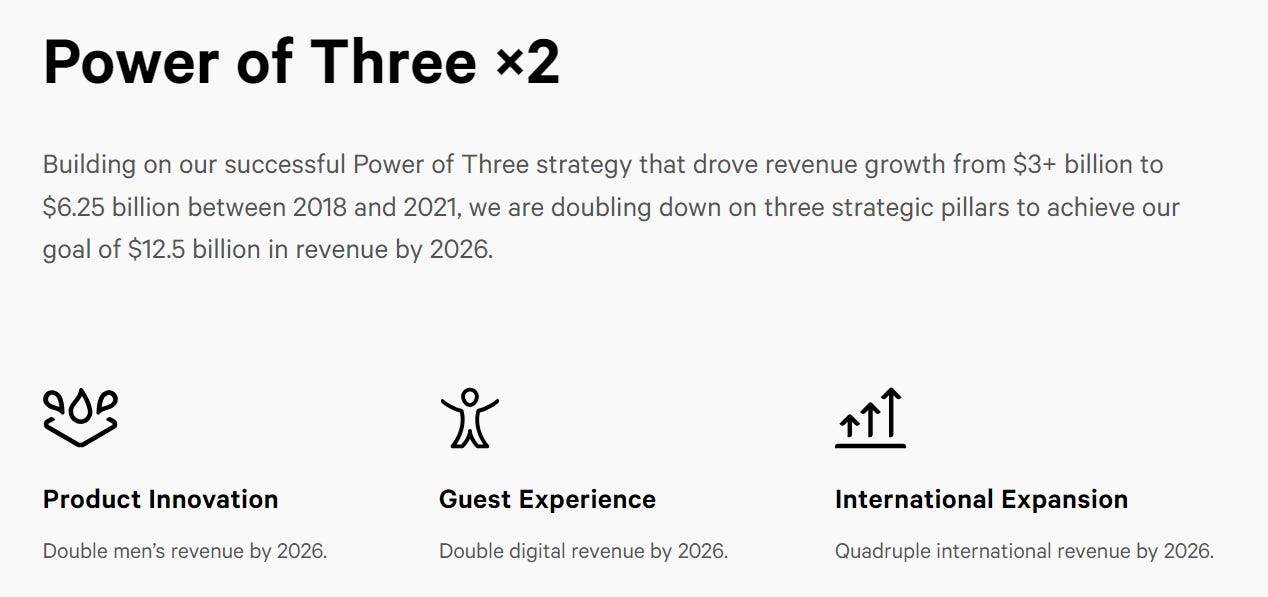

The ‘Power of 3’ 2.0: back in 2021, Management announced a new roadmap to double sales and hit $12.5 billion by 2026.

To achieve this, the company layed out some specific growth levers:

Sharp rise of the men’s segment

Steep increase of digital revenues

Massive International Expansion plans

50%-50%: the geographical breakdown - North America vs Rest of the World - of Sales that Management considers possible for the years to come.

For the full year 2023, international was only 21% of our business and over the long run, I see the potential for it to grow to 50% as we continue to expand our presence outside of North America.

Calvin McDonand - CEO of Lululemon - during latest earnings call.

This sounds ambitious, doesn’t it?

To be fair tough, it would not be the first time Management hits significant milestones, as they were able to bring revenues from $3bn to more than $6bn between 2018 and 2021.

Yet if this is supposed to be pretty realistic, why is Mr. Market negative on the stock? Is he wrong? Are we in front of a compelling opportunity?

Let’s find out starting by seeking quality first.

Quality Leading Indicators Checklist

As long-time readers may already know, I love researching stocks starting from leading qualitative indicators rather than static financial KPIs (see my article “Stocks Leading Indicators” for a full reference).

It’s a fact more than a coincidence: since I started embracing these concepts as primary source of investment ideas - at the expense of the usual stock screeners - my mistakes radically decreased and my returns were boosted.

Here’s a summary for LULU:

Once again, a score of 2/6 is not a deal breaker. The list should be seen as a starting point to guide effective research and dive deeper on each of these topics.

All in all, I would highligh the following:

Lululemon is a rising Canadian brand with promising international ambitions

Despite being onboard since 2018 only, the CEO seems quite analytical and long-term oriented. Power of 3 1.0 was a huge milestone and a solid proof of execution

Positive NPS confirms the feeling of customer centricity that transpires analyzing the company’s effort and initiatives to retain them.

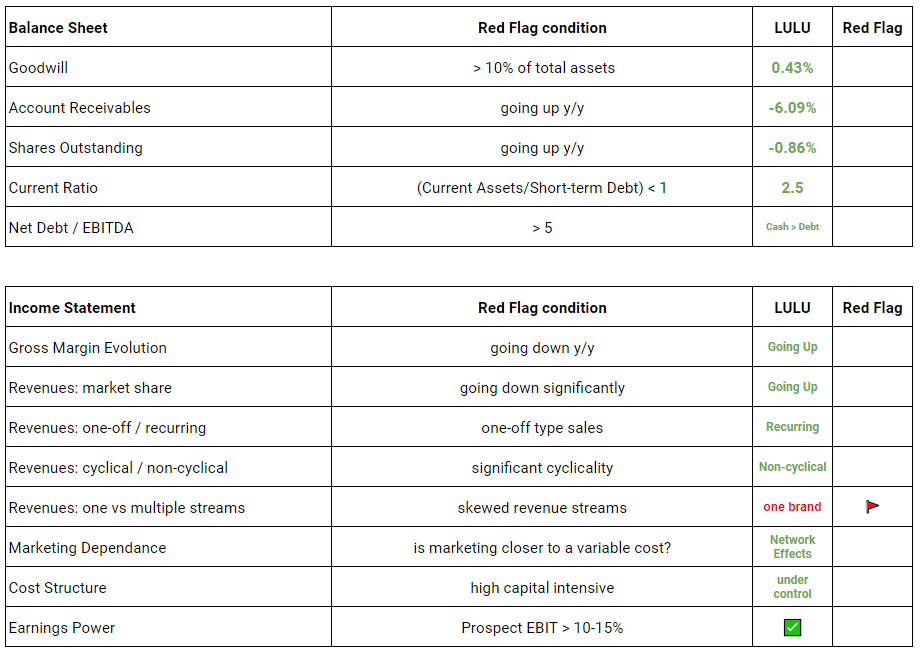

Financial Health & Red Flags

In this paragraph, I will list some of the financial metrics I typically examine to spot for warning signs.

I won't delve deeply into every single metric for the sake of conciseness, but I made the effort to make these tables as intuitive as possible.

In the “condition” column, you will find a brief description of what triggers each red flag.

In summary:

Lululemon exhibits a very solid balance sheet. This is crucial, considering the possibility of further macroeconomic headwinds on the US consumer side

If that was a blind income statement check, I’d never tell this one belongs to a retail business. Margins here are simply amazing.

As such, it does not come as a surprise to witness impressive cash flow and capital allocation ratios.

🚩 The Red Flag: while it is true that the product offering is wide in terms of collections, use cases, and target customers, expert investors should also take into account in my opinion how a single minor trust or reputational issue affecting Lululemon’s brand could negatively impact the whole business at once.

Business Case

At the heart of today’s idea, I’d like to share with you some initial projections on Lululemon in the form of a basic business case.

Here’s what I did:

I focused on Sales Segment by geography - North America, China, and ROW (Rest of the World) - and projected each segment 5 years out

Matched 2028 Sales with hypothetical 2028 Free Cash Flow Margin (from 15% to 20%)

Built a basic Sensitivity Analysis taking into consideration a range of reasonable end FCF Multiples (from 14 to 22)

Duplicated the analysis for 3 scenarios (Bear, Base, Bull), where I play with Sales growth leaving profitability unchanged.

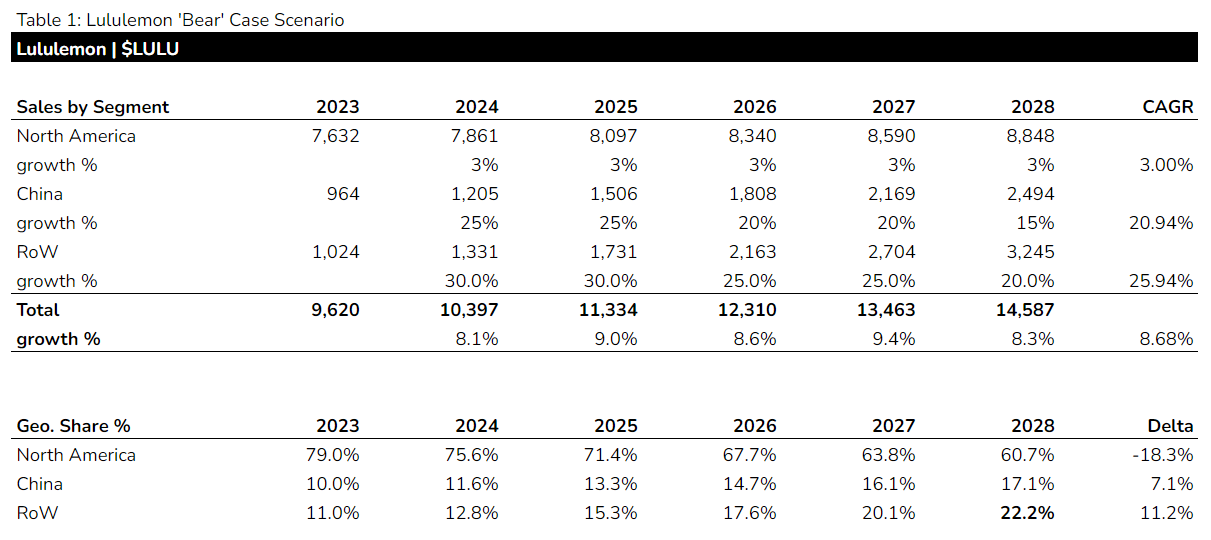

🐻 The Bear Case

In the worst scenario, I assumed the following:

North America Sales growing at a 3% per year, in line with inflation and reflecting consumer weakness and substantial business deceleration

China and ROW growing at a much faster clip (21% and 26% CAGR) accounting for 39% of total sales by 2028

Result: Even in the bear case, Lululemon stock appears to be trading at a fair discount today in light of pretty conservative input assumptions for the next 5 years. Considering an average FCF margin of 17% and a 18 end multiple, it is not crazy to expect a market capitalization of $46 Bn in 2028.

⚖️ The Base Case

In the mid scenario, I assumed the following:

North America Sales growing at a 4.60% per year, reflecting consumer weakness and substantial business deceleration, but above inflation

ROW with massive growth (31% CAGR) accounting, together with China, for 40% of total sales by 2028

Result: Similar to the bear case, these assumptions are not impossible for Lulu. A dramatic deceleation in US & Canada revenue growth, if matched with the anticipated international expansion, would still produce enough FCF to justify a $50 Bn Market Capitalization by 2028 (a +50% from now).

🐂 The Bull Case

In the bull scenario, I assumed one simple idea:

North America Sales growing at 7% per year. Everything else unchanged.

Result: Simple. A minor change in domestic sales growth determines material change in returns expectations. My take is: is Management trying to deviate the attention to international markets, while knowing exactly that domestic presence is still far more important and too big to ignore?

➡️ I come out from this first analysis with a clear conviction. US Sales growth is still the most important number to look at.

The 100% Recipe

None of the 3 scenarios seems to reasonably produce a 100% return in 5 years (well, yes they do but a bit streched).

What needs to happen for you to double your money with Lulu stock?

Reverse DCF (Simplified)

As you see in the data below, Lululemon should be able to grow revenues at an average pace of 17% per year, if a 18% FCF margin and a 18 FCF multiple make sense for 2028.

In our Bull Case above, the Sales CAGR hit 12% only, thus indicating how a reacceleration would be needed for Mr. Market to turn bullish on LULU again.

Buy Target Prices from Today

Alternatively, you can just wait and see if Lululemon keeps dropping (never hope too much for this kind of things though!).

What stock price would more likely increase the chances of a 2x, keeping all the other variables and business fundamentals unchanged?

Taking the expected Market Capitalizations from the 3 scenarios, we can roughly conclude how another -20%/-25% price drop from now would present an even more compelling upside opportunity. If fundamentals do not change in between.

Conclusion

I don’t own Lululemon stock. I am only planning to continue my research in the following directions:

Further analyze revenue growth by Digital vs In-Store Sales

Understanding potential earnings power

Evaluate if there are further upselling or cross-selling opportunities to make domestic sales reaccelerate

In terms of final risk reward for today, I like the fact that the downside does seem protected. At the same time, I tend to prefer companies with higher earnings power and upside potential. Maybe this is also the case and I haven’t got it yet: and that’s how my research will continue.

💡 Are you bullish or bearish on Lululemon? I am all ears in the comments!

Let’s make Business Invest grow!

📢 If you find value in my episodes, feel free to restack, like, or comment below.

For any ideas or request, feel free to reach out via DM.

📈

Thank you again for your valuable time.

Happy Investing,

Francesco - Business Invest

Thanks a lot for such a detailed analysis! I think that $LULU has a good position right now. Wrote my analyses as well - https://longtermpick.com/p/lululemon-analysis

I own some shares and going to add more soon 😺

I have Lululemon in my watchlist for a long-time and ready to jump on board when i see momentum turn positive.