4 Cyber-Securities To Watch

4 Cyber-Securities To Watch

And some thoughts about their next 5 years 💸

Data doesn’t lie:

10.7%: the expected CAGR of the US Cybersecurity Industry for 2024 -2030 (grandviewresearch.com)

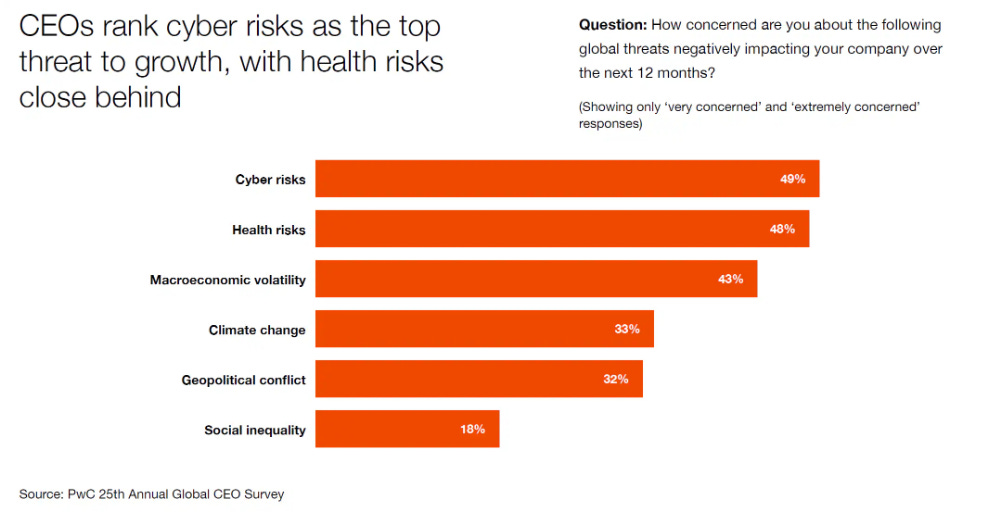

49%: the percentage of global CEOs being ‘very concerned’ or ‘extremely concerned’ about cyber attacks - highest global threat (PwC 25th Global CEOs Survey)

60%: the percentage of global Risk Manager perceiving Cyber as the main operational risk in 2024 (strategic-risk-global.com)

…Cybersecurity is a thing.

💡 In Today’s episode I’ll be sharing some preliminary insights from taking a first leap into this new and fascinating industry for me.

➡️ In particular, I’ll be screening 4 cybersecurity profiles and test their 5-year risk-reward profile.

Ready?

A Blue Ocean Industry

I would define Cybersecurity as the perfect example of a Blue Ocean industry, where:

Demand is rising with no sign of maturity

Products and service are need-based

There is space for multiple winners

Competition is value-driven and not on price

Cost-structure is favorable and provide companies enough margin of safety

Innovation standards are high

So, to visualize it, you have 1) a growing industry:

… 2) clearly need based:

… with a fragmented competitive landscape (multiple winners):

I definitely like it.

And I would not mind positioning myself in such a ‘safe’ industry should the market enter a correction territory after an extensive bull-run.

That being said, nothing is safe in the stock market and that is why it is crucial to distinguish case by case what the market is serving to our table as we speak.

👇🏼

Cyber-Stocks: Overview

Palo Alto Networks, CrowdStrike, Fortinet, ZScaler, Cloudflare.

Some common patterns emerge from comparing these industry leaders:

Very solid and resilient revenue growth, between 25% and 50% on average per year. Here I took the 3-year CAGR, but they have actually been growing at this pace for way more than that.

Discrepancy between profit margins and free cash flow margins: profits seem to be capped by common non-monetary expenses such as license amortizations and stock-based compensation expenses. This shows the potential for future earnings optimization once these expenses will eventually start fading away and profit margins may catch up to free cash flow margins.

Almost all of these companies are still diluting shareholders, which is something we don’t want to see. Fortinet is the exception.

Almost all of them are still led by their historical Founders, which is something we love to see.

External growth through acquisitions is pursued aggressively and it may be also reflected into the Goodwill, which in some cases exceed our 10% threshold.

Check-up Valuation Framework: disclaimer

In this first article, I explained how I intend to use this framework for my analyses, but it may be the case to refresh a few rules of the game once again:

Valuation itself means nothing and I never buy or sell based on this tool. It only represents one step of a broader investing process;

I use this framework: a) a time saver to quickly test the attractivity of a stock from a valuation standpoint, and b) after I’m done with business fundamentals to finally test the most reasonable risk-reward profile.

Today’s stocks projections represent projections based on premilinary unfinished research I’ve done on the following companies

The goal is to trigger further discussion and this is never financial advice. Make sure to conduct your own research.

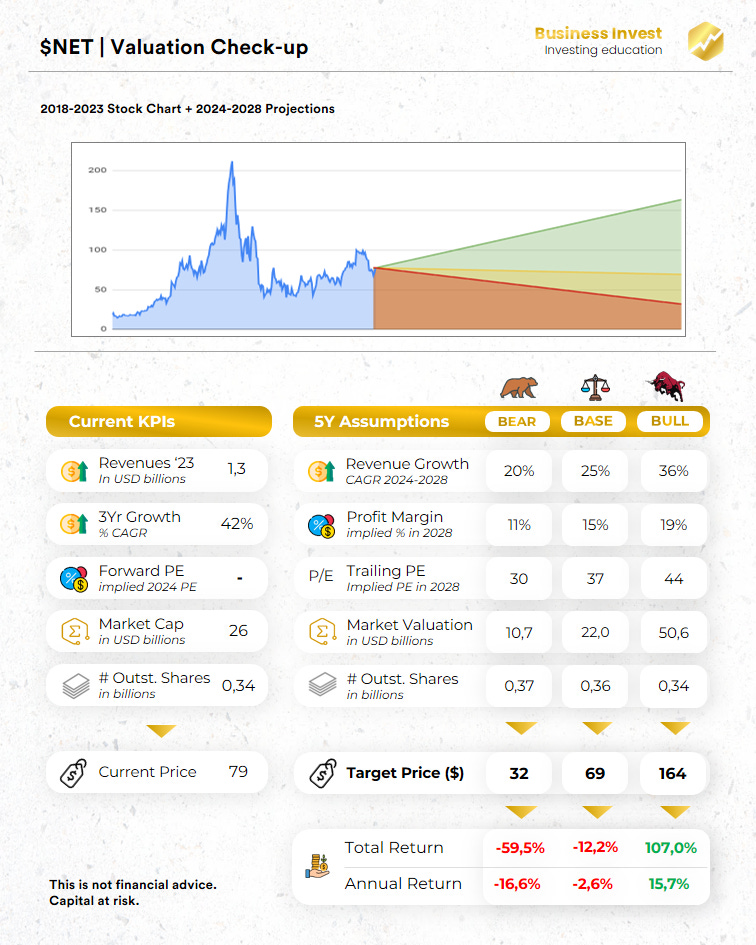

NET 0.00%↑ Cloudflare

Among the 4 companies I’ll be quickly going through, Cloudflare is the one with the lowest free cash flow margins and the company has been losing money since I can remember.

So, I asked myself: what should happen for the stock price to double from current levels?

Management should maintain revenue growth rates almost stable - assuming 36% for the next 5 years: that’s a lot;

Profit margins should approach 20%

The market should reflect positive sentiment on a fast growing, profitable stock with an end-multiple of 44 times earnings.

This is feasible if Management keeps executing like they have been in the past, but I must reckon how execution must be perfect from now on and that’s not a position I want to be in as long-term investor.

Plus, unprofitable companies will be the first ones to fall sharply should the stock market start a correction period in the next few months.

⚙️ The Key Assumptions

Company executes and scale to reach profitable growth

End-multiples reflecting scalability, growth rates, software-type valuations and sentiment

Dilution still hurting shareholder base

➡️ I may be totally wrong here, but the risk-reward does not satisfy me.

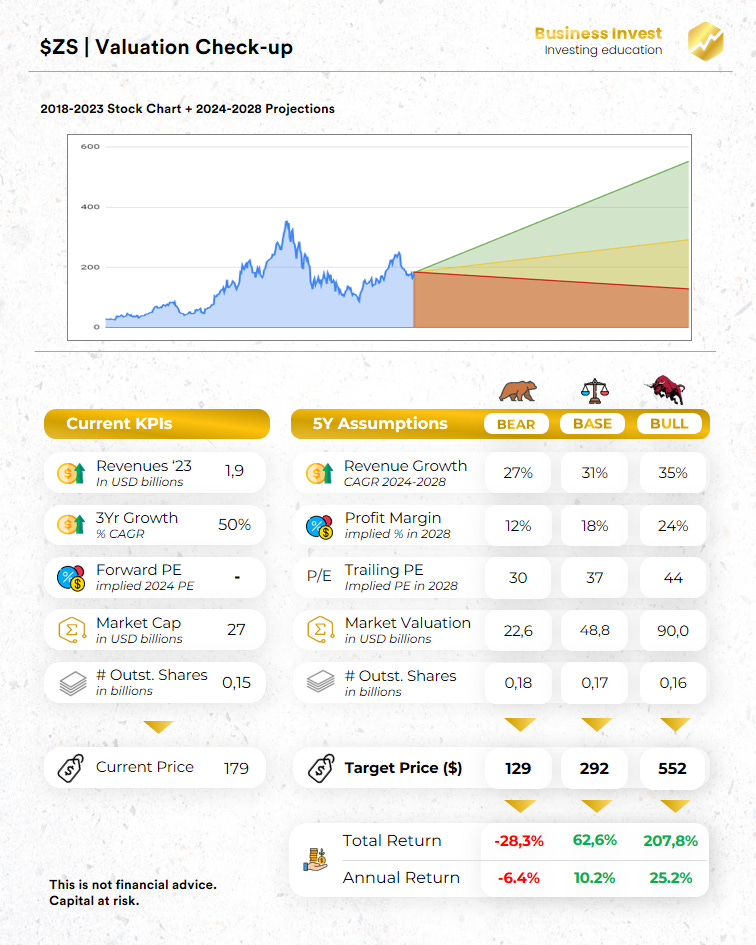

ZS 0.00%↑ ZScaler

In this group, Zscaler is the fastest growing business with the highest Insider Ownership percentage. But that’s not all:

It exhibits the highest discrepancy between FCF and profits: +29% vs -3.5%;

Unlike Cloudflare, losses have been decreasing over the last few quarters. Are we close to a breakeven point?

The company is specialized in Cloud, which I like a lot.

⚙️ The Key Assumptions

Growth decelerates compared to current levels

The company reaches profitable growth but never matches current Free Cash Flow margins (that’s somehow conservative)

End-multiples reflecting scalability, growth rates, software-type valuations and sentiment

➡️ The price range brought up by the framework is quite wide but the initial risk-reward seems interesting. I will be closely monitor ZS.

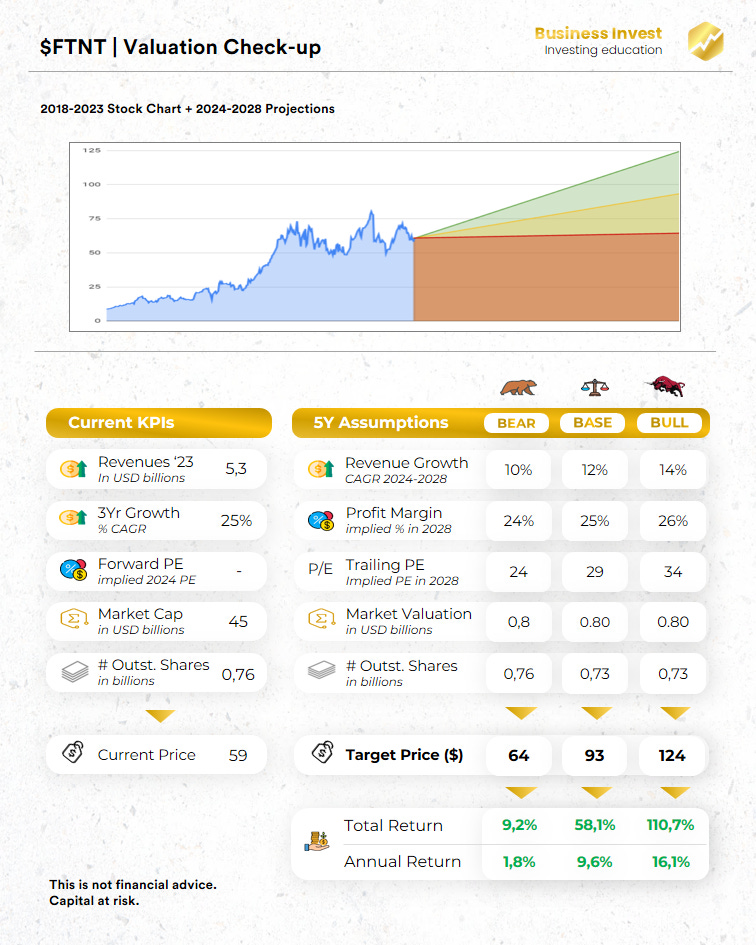

FTNT 0.00%↑ Fortinet

Fortinet is the least growing company in the group (they’re growing ‘only’ 25% per year since 5 years). That being said, the profile is very interesting:

17% insider ownership and Founder-Led

Goodwill well under control - it means Management is brilliant in conducting M&A

31% Free Cash Flow Margin

Shares Buyback at -2% rate per year

⚙️ The Key Assumptions

Growth decelerates and goes in line with the overall industry - that’s conservative

The company maintains profitable growth but never matches current Free Cash Flow margins (that’s also somehow conservative)

End-multiples reflecting a more mature, software-based, business

➡️ Fortinet exhibits a very interesting risk-reward. While it does not impress me in terms of upside potential, I like it a lot if I think about positioning myself defensively in the current stock market. Remember W. Buffett rule n.1: never lose money!

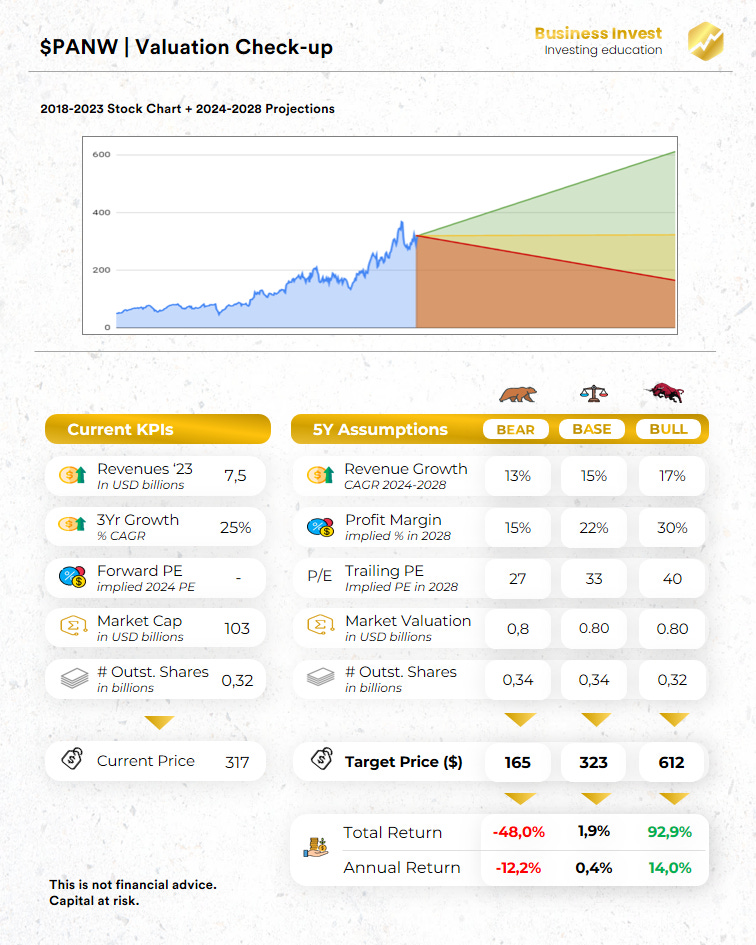

PANW 0.00%↑ Palo Alto Networks

Disclaimer: Palo Alto is the one I am less informed about and I still have to fine-tune my research.

As such, I plugged in some input varibales based on past performance and here’s what the framework tells me:

It tells me that anything can happen on this one.

⚙️ The Key Assumptions

Growth decelerates and goes in line with the overall industry - as for FTNT, that’s conservative

The company maintains profitable growth but never matches current Free Cash Flow margins of 38% - the best in the group (that’s also somehow conservative)

End-multiples reflecting a dominant leader in a software-based industry

➡️ I cannot express myself on this one before I understand something more on the business fundamentals of the company.

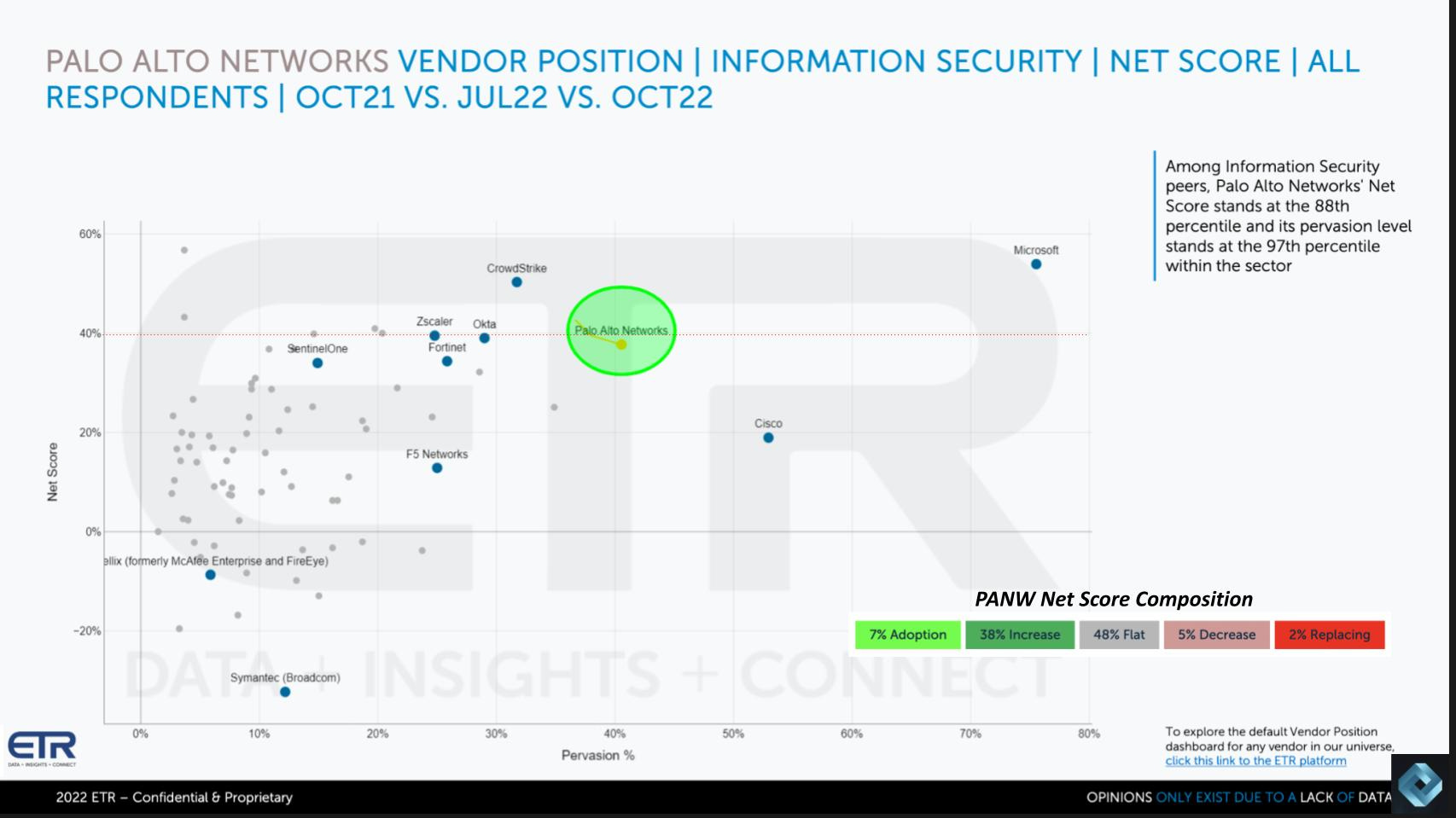

From that perspective, I would like to mention an insightful article by The Cube Research (link here) that explains really well some dynamics regarding Palo Alto and their competitive advantage.

Just to anticipate, they developed a particular score tracking the Customer Loyalty and Network Effects within the Cybersecurity competitive landscape. Definitely worth checking out!

Let’s make Business Invest Newsletter grow!

Sharing my investing journey on Substack genuinely has been bringing lots of fun & fullfilment over these first few months.

📢 If you find value in my episodes, feel free to restack, like, or comment below.

If you’re an expert about the Cybersecurity industry or would like to learn more about it together: feel free to reach out via DM and we’ll discuss further!

📈

Thank you again for your valuable time.

Happy Investing,

Francesco - Business Invest

Very well explained. Thanks once again